A Traders’ Week Ahead: U.S.–China Trade Talks, Mega-Cap Earnings, and Global Central Bank Decisions

Donald Trump’s Asia tour takes centre stage this week, with global markets fixated on his highly anticipated meeting with Chinese President Xi Jinping on Thursday.

Resuming large-scale purchases of U.S. soybeans

Demonstrating stronger enforcement on fentanyl supply chains

Reports from the weekend meeting between Scott Bessent and the Chinese Vice President indicate that a deal has been finalised, with the conditions outlined above met and set to be formally announced following the Trump–Xi meeting on Thursday. Markets had largely viewed this as the higher-probability outcome, so the news won’t come as a major surprise and is partly priced. That said, relief buying could still put upside risk into the CN50, NAS100, AUD, and other risk-sensitive assets through the trading week.

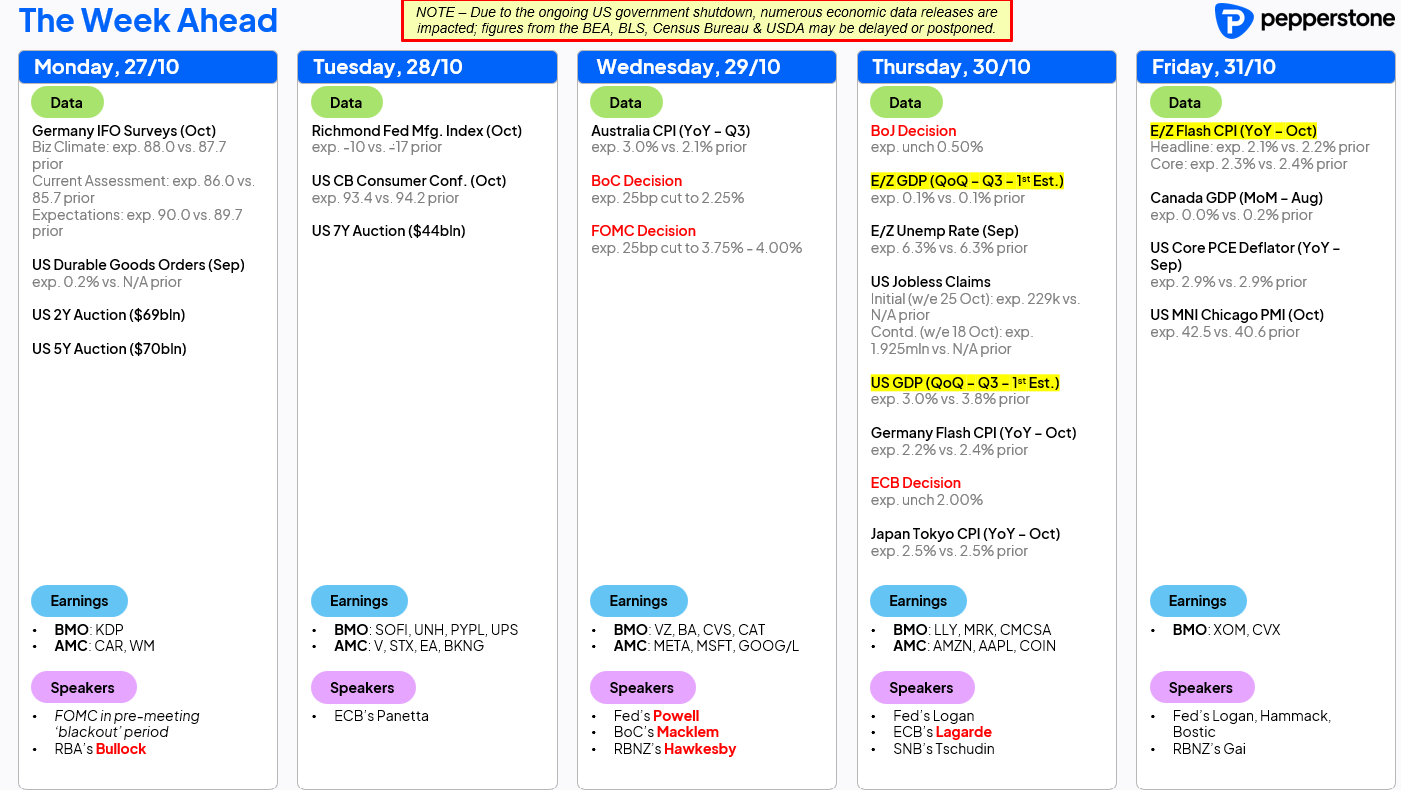

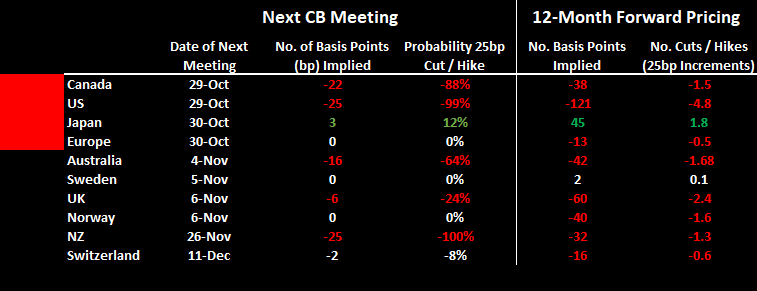

A huge week for global monetary policy as four major G10 central banks — the Federal Reserve, Bank of Canada, European Central Bank, and Bank of Japan — hold meetings. Fed & BoC: Interest-rate swaps imply a 25bp rate cut from each. ECB & BoJ: Both are expected to hold policy steady. The BoC meeting offers the greatest potential surprise versus market pricing, though the FOMC meeting will command global trader attention.

The Federal Reserve is widely expected to cut the Fed funds rate by 25 basis points, with almost no market pricing for an alternative outcome.

The focus will also be on whether the Fed formally ends its Quantitative Tightening (QT) program or signals it will wind it down in coming months.

In his press conference, Chair Jerome Powell will likely avoid committing to another 25bp cut at the December meeting, given the Fed would essentially have three months of new data to consider by that meeting, as well as potentially important developments on the trade front.

In the EM space, the Central Bank of Chile (BCCh) meets on Tuesday. After a hotter-than-expected September CPI print, policymakers are widely expected to hold rates at 4.75%. With the Chilean election looming in November, traders remain constructive on the Chilean peso (CLP) — the USDCLP fell 1.7% last week and momentum offers a probability that the pair could drift lower into the meeting.

It’s the busiest week of the quarter for U.S. earnings, with around 45% of S&P 500 market cap reporting.

A point of note, Meta, Microsoft, and Alphabet release results two hours after the FOMC meeting — setting up a higher-volatility period for equities in the after-market period, and the NAS100 and US500.

Retail-trader favourites Coinbase, Reddit, and Riot Platforms also report Thursday.

US Q3 Earnings: The State of Play so far

Negotiations between Republicans and Democrats remain deadlocked, with no clear path yet to re-open the government. Rising health-insurance premiums under the Affordable Care Act (ACA) on 1 November are adding urgency, as Democrats aim to avoid further cost pressures.

A critical data point for AUD and AUS200 traders — Wednesday’s Q3 CPI will shape expectations ahead of the RBA’s 4 November meeting (cash rate currently 3.6%).

Trimmed Mean CPI: +0.8% q/q, +2.7% y/y

Possible Scenarios:

+0.9% q/q: The market likely prices a 50% probability of a 25bp cut in November.

1.0% q/q or higher: RBA likely holds rates steady at 3.6% in November.

The pain trade is for Aussie Q3 TM CPI come in at 0.9%+, which would result in the AUD staging a solid rally (notably vs the cross rates) and the AUS200 lower by 0.8%+.

Nvidia hosts its annual AI developers’ conference this week, with CEO Jensen Huang delivering his keynote on Tuesday (12 p.m. ET). Historically, GTC has been a catalyst for AI stocks and semiconductor optimism, as investors react to innovation themes and forward-looking product announcements.

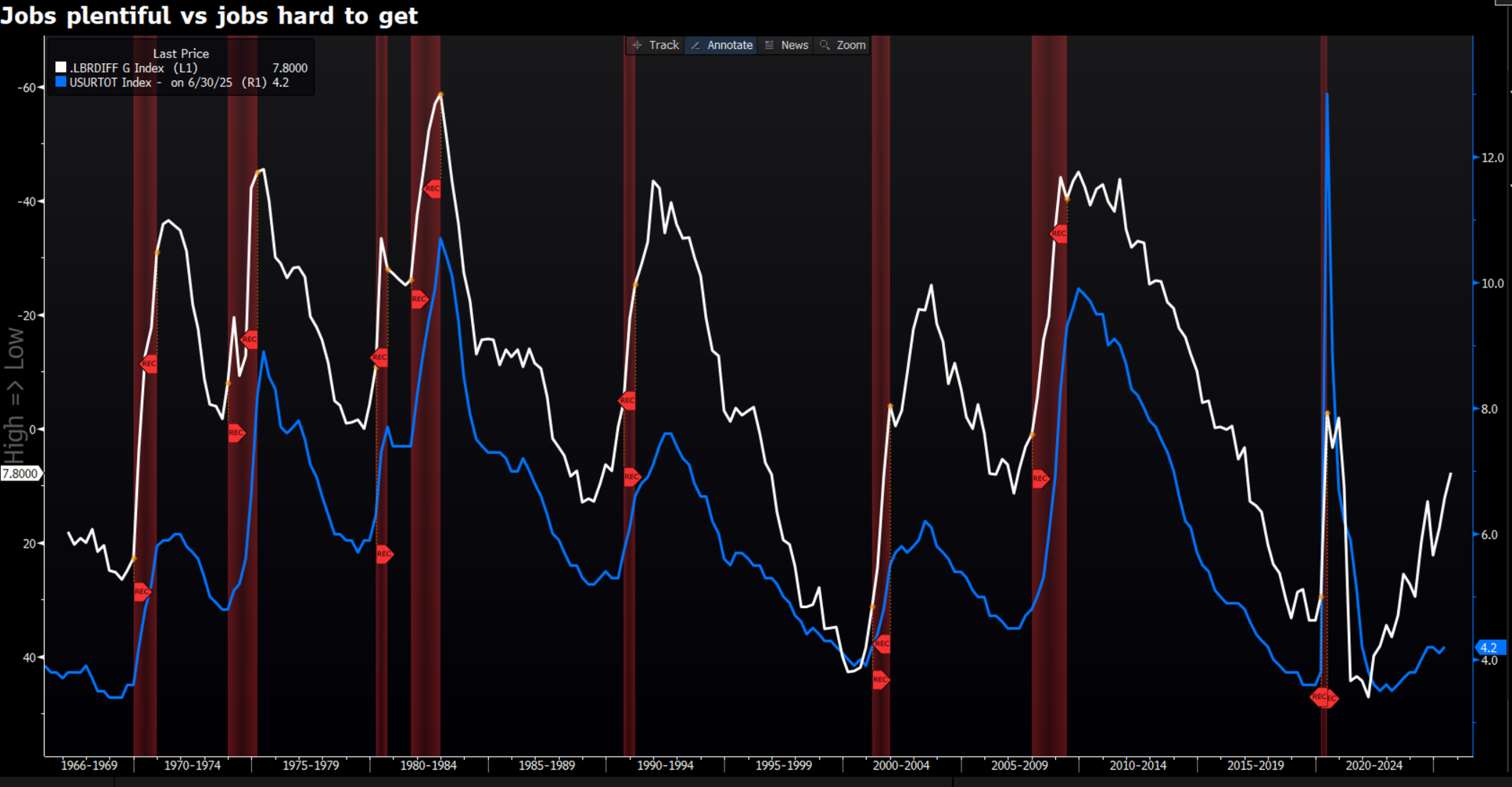

Labour Market Signal While not typically a volatility driver, the Conference Board Consumer Confidence Index offers a crucial insight — the “Jobs Plentiful vs. Jobs Hard to Get” spread, also known as the Labour Market Differential. This metric has historically led trends in U.S. unemployment rate. With “Jobs Hard to Get” now at its highest level since Feb 2021, traders may interpret it as a leading indicator of rising unemployment — and potential dovish tilt in Fed expectations.

This week presents one of the most event-heavy line-ups for risk events of the year — where macro policy, tech earnings, and political risk all intersect.

Disclaimer:

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn't represent that the material provided here is accurate, current or complete, and therefore shouldn't be relied upon as such. The information, whether from a third party or not, isn't to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers' financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn't permitted.

Publication date: